Introduction-

Understanding the balance sheet isn’t just for accountants—it’s a fundamental skill for every business owner, banker, and investor. This powerful tool reveals the financial health of a firm, guiding critical decisions on liquidity, sustainability, and growth. In my latest blog, I break down the golden rules of aligning short-term and long-term sources with their respective applications, explore common pitfalls, and share actionable insights for bankers analyzing customer balance sheets. Stay informed to safeguard your financial strategies!

————————————————————————————————————————————-

A firm’s balance sheet serves as a critical snapshot of its financial health at any given point in time. It is an essential tool for business owners, investors, and stakeholders to assess the company’s stability and operational efficiency. The balance sheet is broadly divided into two categories: short-term and long-term components. Each plays a pivotal role in shaping the firm’s financial structure.

The Two Parts of the Balance Sheet

- Short-Term Sources and Applications: Short-Term Sources: These include liabilities and borrowings that need to be settled within a year, such as trade payables, short-term loans, and accrued expenses. Short-Term Applications: These represent assets that can be converted into cash within a year, such as inventories, trade receivables, and cash equivalents.

- Long-Term Sources and Applications: Long-Term Sources: These include equity, reserves, and long-term borrowings that provide a stable financial foundation. Long-Term Applications: These represent fixed assets, investments, and other resources used for sustaining the business over a longer horizon.

Golden Rule of Financial Management

To maintain a balanced financial structure, it is imperative to:

- Utilize short-term sources exclusively for short-term applications.

- Allocate long-term sources towards long-term applications.

Deviating from this principle can have significant implications:

- Using Short-Term Sources for Long-Term Applications: This creates a Negative Net Working Capital (NWC) scenario where short-term liabilities (STL) exceed short-term assets (STA). The firm may face liquidity challenges, as immediate obligations cannot be met without difficulty.

- Using Long-Term Sources for Short-Term Applications: This leads to a Higher Net Working Capital, with short-term liabilities being lower than short-term assets (STL < STA). While this indicates a stronger financial buffer, it also reflects inefficient use of long-term funds, reducing returns on equity.

Common Pitfalls in Balance Sheet Management

A frequent mistake among business owners is the misallocation of funds. In their effort to address immediate business requirements, they often divert long-term sources toward short-term applications or vice versa. This diversification can deteriorate the balance sheet, leading to poor financial performance and a potential loss of stakeholder trust.

For instance:

- Over-reliance on short-term borrowings to finance long-term assets can lead to a cash crunch.

- Using long-term funds for short-term expenses might tie up resources that could otherwise generate higher returns in the long run.

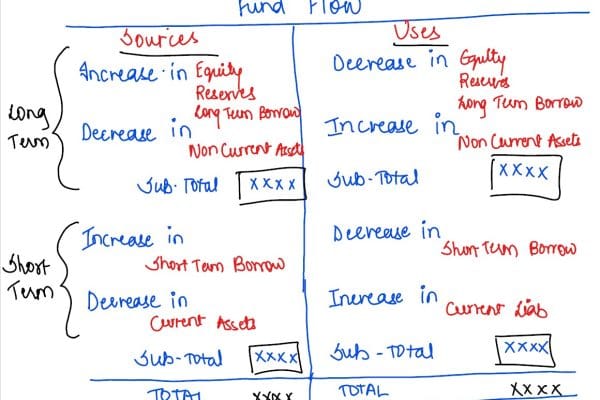

Visualizing the Balance Sheet

A pictorial representation as depicted above, can help simplify the understanding of balance sheet dynamics. By categorizing assets and liabilities into short-term and long-term buckets, one can easily visualize mismatches and evaluate the firm’s financial equilibrium.

Conclusion

A well-managed balance sheet is the cornerstone of a successful business. By adhering to the principle of aligning sources with their respective applications, firms can:

- Ensure liquidity and solvency.

- Enhance operational efficiency.

- Build trust among stakeholders.

Business owners must prioritize disciplined fund management and regularly review their balance sheets to avoid common financial pitfalls. A balanced and well-structured financial strategy not only safeguards the firm’s immediate needs but also secures its long-term growth trajectory.

Precautions for Bankers

When analyzing balance sheets of customers, bankers must:

- Assess Alignment: Verify whether short-term and long-term sources are appropriately aligned with their respective applications.

- Examine Liquidity Ratios: Review current and quick ratios to ensure the customer can meet immediate obligations.

- Evaluate NWC Trends: Look for patterns of negative or excessively high NWC that may indicate mismanagement of funds.

- Understand Cash Flow: Analyze cash flow statements to confirm the sustainability of the customer’s financial operations.

- Scrutinize Borrowings: Ensure that short-term borrowings are not being used for long-term investments, which could strain liquidity.

- Monitor Diversification: Be cautious of over-diversification of funds that could lead to inefficiencies or financial instability.

By adopting a thorough and structured approach, bankers can make informed decisions, mitigate risks, and provide value-added guidance to their customers.

Hereby invite comments on situations, where such diversification has landed the customer in trouble / deteriorated the growth graph.